Free Connecticut 8379 PDF Template

Free Connecticut 8379 PDF Template

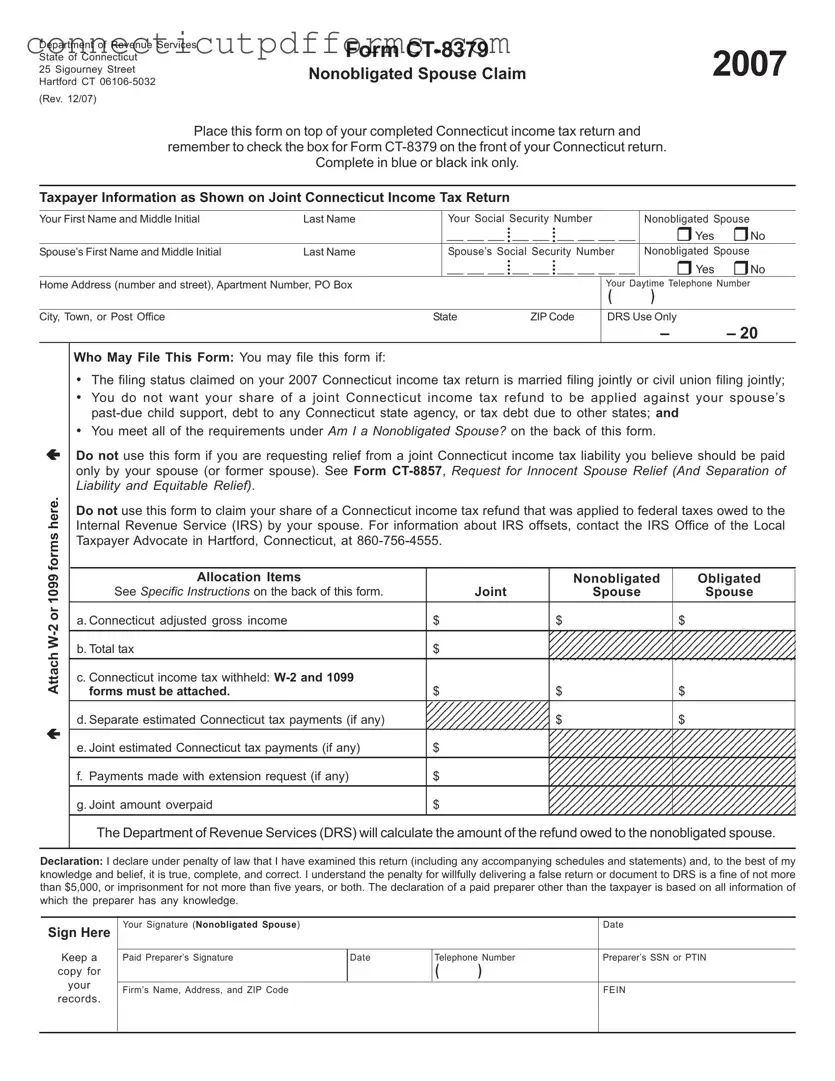

The Connecticut 8379 form, officially known as the Nonobligated Spouse Claim, serves a specific purpose for taxpayers who find themselves in a unique situation during tax season. This form is designed for individuals who filed a joint Connecticut income tax return but want to ensure that their share of any tax refund is not applied to their spouse's outstanding debts, such as past-due child support or tax obligations owed to other states. By completing this form, the nonobligated spouse can claim their rightful portion of a tax refund, provided they meet certain eligibility criteria. These criteria include having no debts themselves that would warrant a refund offset and having contributed to the joint tax return through income or tax payments. The form requires detailed taxpayer information, including Social Security numbers and income allocations, ensuring that the Department of Revenue Services can accurately calculate the refund owed to the nonobligated spouse. It’s important to attach necessary documentation, such as W-2s or 1099 forms, to support the claim. Overall, the Connecticut 8379 form provides a structured way for nonobligated spouses to assert their rights while navigating the complexities of joint tax filings.

Ct Realtors - This is a formal agreement outlining the purchase and sale of real property.

The necessary Employment Verification documentation is vital for employers to ensure their staff meets the required eligibility standards for employment in New Jersey.

Ed049F - Ineligible construction costs must be itemized clearly on the form.

| Fact Name | Details |

|---|---|

| Form Purpose | This form allows a nonobligated spouse to claim their share of a joint Connecticut income tax refund that may be applied against their spouse's debts. |

| Eligibility Criteria | To file, you must be married filing jointly and not owe any past-due child support or debts to Connecticut state agencies. |

| Filing Instructions | Place Form CT-8379 on top of your completed Connecticut income tax return and check the box for this form on the front of your return. |

| Required Attachments | Attach copies of all W-2 and 1099 forms showing Connecticut income tax withheld to Form CT-8379. |

| Governing Law | This form is governed by Connecticut General Statutes, specifically regarding tax refunds and obligations of spouses. |

| Signature Requirement | The nonobligated spouse must sign the form. A paid preparer must also sign if the return is prepared by someone else. |

Department of Revenue Services

State of Connecticut

25 Sigourney Street

Hartford CT

(Rev. 12/07)

Form |

2007 |

Nonobligated Spouse Claim |

Place this form on top of your completed Connecticut income tax return and

remember to check the box for Form

Complete in blue or black ink only.

Taxpayer Information as Shown on Joint Connecticut Income Tax Return

Your First Name and Middle Initial |

Last Name |

|

Your Social Security Number |

|

Nonobligated Spouse |

|||

|

|

|

• |

• |

__ __ __ __ |

Yes |

No |

|

|

|

|

__ __ __ •• |

__ __ •• |

||||

|

|

|

• |

• |

|

|

Nonobligated Spouse |

|

Spouse’s First Name and Middle Initial |

Last Name |

|

Spouse’s Social Security Number |

|||||

|

|

|

• |

• |

__ __ __ __ |

Yes |

No |

|

|

|

|

__ __ __ •• |

__ __ •• |

||||

|

|

|

• |

• |

|

|

|

|

Home Address (number and street), Apartment Number, PO Box |

|

|

|

|

Your Daytime Telephone Number |

|||

|

|

|

|

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

City, Town, or Post Office |

|

State |

ZIP Code |

DRS Use Only |

|

|||

|

|

|

|

|

|

|

– |

– 20 |

Attach

Who May File This Form: You may file this form if:

•The filing status claimed on your 2007 Connecticut income tax return is married filing jointly or civil union filing jointly;

•You do not want your share of a joint Connecticut income tax refund to be applied against your spouse’s

•You meet all of the requirements under Am I a Nonobligated Spouse? on the back of this form.

Do not use this form if you are requesting relief from a joint Connecticut income tax liability you believe should be paid only by your spouse (or former spouse). See Form

Do not use this form to claim your share of a Connecticut income tax refund that was applied to federal taxes owed to the Internal Revenue Service (IRS) by your spouse. For information about IRS offsets, contact the IRS Office of the Local Taxpayer Advocate in Hartford, Connecticut, at

|

Allocation Items |

|

Nonobligated |

Obligated |

|

See Specific Instructions on the back of this form. |

Joint |

Spouse |

Spouse |

|

|

|

|

|

|

a. Connecticut adjusted gross income |

$ |

$ |

$ |

|

|

|

|

|

|

b. Total tax |

$ |

|

|

|

|

|

|

|

|

c. Connecticut income tax withheld: |

|

|

|

|

forms must be attached. |

$ |

$ |

$ |

|

|

|

|

|

|

d. Separate estimated Connecticut tax payments (if any) |

|

$ |

$ |

|

|

|

|

|

|

e. Joint estimated Connecticut tax payments (if any) |

$ |

|

|

|

|

|

|

|

|

f. Payments made with extension request (if any) |

$ |

|

|

|

|

|

|

|

|

g. Joint amount overpaid |

$ |

|

|

|

|

|

|

|

The Department of Revenue Services (DRS) will calculate the amount of the refund owed to the nonobligated spouse.

Declaration: I declare under penalty of law that I have examined this return (including any accompanying schedules and statements) and, to the best of my knowledge and belief, it is true, complete, and correct. I understand the penalty for willfully delivering a false return or document to DRS is a fine of not more than $5,000, or imprisonment for not more than five years, or both. The declaration of a paid preparer other than the taxpayer is based on all information of which the preparer has any knowledge.

Sign Here

Keep a

copy for

your

records.

Your Signature (Nonobligated Spouse) |

|

|

|

Date |

|

|

|

|

|

Paid Preparer’s Signature |

Date |

Telephone Number |

Preparer’s SSN or PTIN |

|

|

|

( |

) |

|

|

|

|

|

|

Firm’s Name, Address, and ZIP Code |

|

|

|

FEIN |

|

|

|

|

|

|

|

|

|

|

Form

Purpose: Use Form

•You are a nonobligated spouse and all or part of your overpayment was (or is expected to be) applied against:

•Your spouse’s past due State of Connecticut debt (such as child support, student loan, or any debt to any Connecticut state agency); or

•A tax debt due to other states; and

•You want your share of the joint overpayment refunded to you.

Any reference in this document to a spouse also refers to a party to a civil union recognized under Connecticut law.

General Instructions

Am I a Nonobligated Spouse?

You are a nonobligated spouse, if you meet all of the following requirements:

•You filed a joint Connecticut income tax return with a spouse who owes

•You received income (such as wages, interest, etc.) reported on the joint return;

•You made Connecticut income tax payments (such as withholding or estimated tax payments) reported on the joint return;

•You do not owe

•You filed a joint return reporting an overpayment of Connecticut income tax, all or part of which was or is expected to be applied against

Filing the Return: You must file Form

You must place this form on top of the completed Connecticut income tax return. If you previously filed your 2007 Connecticut income tax return, mail this form separately to: Department of Revenue Services, PO Box 5035, Hartford CT

Important: Attach copies of all forms

showing Connecticut income tax withheld to Form CT- 8379.

Specific Instructions

Taxpayer Information: Enter the taxpayer information exactly as it appears on your Connecticut income tax return. The name and Social Security Number (SSN) entered first on the joint tax return must also be entered first on Form

Allocation Items

a.Connecticut adjusted gross income: Enter the joint amount as reported on your joint Connecticut income tax return (Form

Nonresidents and

Nonresidents and |

Connecticut Source Income |

|

(Form |

||

Only |

||

|

Allocation Item

Joint

Nonobligated Spouse

Obligated Spouse

b.Total tax: Enter the joint Connecticut tax liability as reported on your joint Connecticut income tax return (Form

c.Connecticut income tax withheld: Enter the joint Connecticut withholding as reported on your joint Connecticut income tax return (Form

d.Separate estimated Connecticut tax payments: Enter any separately paid estimated Connecticut income tax payments in the appropriate spaces.

e.Joint estimated Connecticut tax payments: Enter the total amount of any joint estimated Connecticut income tax payments. Include overpayments applied from a previous year.

f.Payments made with extension request: Enter the joint amount as reported on your joint Connecticut income tax return (Form

g.Joint amount overpaid: Enter the joint amount overpaid as reported on your joint Connecticut income tax return (Form

Nonobligated Spouse Refund: DRS will calculate the amount of the nonobligated spouse’s refund. The nonobligated spouse’s share of the joint Connecticut tax overpayment cannot exceed the joint overpayment.

Signature: The nonobligated spouse must sign this form.

Others Who May Sign for the Nonobligated Spouse: Anyone with a signed Power of Attorney may sign on behalf of the nonobligated spouse. Attach a copy of the Power of Attorney.

Paid Preparer’s Signature: Anyone you pay to prepare your return must sign and date it. Paid preparers must also enter their SSN or Personal Tax Identification Number (PTIN), and their firm’s Federal Employer Identification Number (FEIN) in the spaces provided.

Form

Filling out the Connecticut 8379 form can be a straightforward process, but many individuals encounter common mistakes that can delay their claims or lead to complications. One prevalent error is failing to include the necessary documentation. Attachments such as W-2 or 1099 forms are crucial as they provide proof of income and tax withheld. Without these documents, the Department of Revenue Services may not process the claim, resulting in unnecessary delays.

Another mistake often made is incorrect or inconsistent information regarding taxpayer details. It is essential to ensure that the names and Social Security Numbers (SSNs) match exactly as they appear on the joint Connecticut income tax return. Any discrepancies can cause confusion and may lead to rejection of the claim. Therefore, double-checking this information before submission can save time and hassle.

Moreover, many individuals overlook the requirement to check the box for Form CT-8379 on the front of their Connecticut income tax return. This simple step is vital as it alerts the processing department to the inclusion of the nonobligated spouse claim. Neglecting to do so can result in the form being misfiled or ignored altogether.

Completing the allocation items section also presents challenges for some filers. It is important to accurately report the Connecticut adjusted gross income and tax amounts for both spouses. Miscalculations or incorrect allocations can lead to incorrect refund amounts. Take the time to carefully review these figures and ensure they correspond with the joint return.

Lastly, failing to sign the form is a critical error that can halt the entire process. The nonobligated spouse must sign the CT-8379 to validate the claim. If someone else prepares the form, their signature is also required. Remember, a missing signature can delay the processing of the claim, so it is vital to ensure that all necessary signatures are in place before submission.

When filling out the Connecticut 8379 form, there are several important points to keep in mind to ensure the process goes smoothly. Here are key takeaways:

The Connecticut 8379 form is similar to the IRS Form 8379, which is the Injured Spouse Claim and Allocation. Both forms serve to protect one spouse from the financial liabilities of the other. In the case of the IRS form, it allows a spouse to claim their portion of a tax refund that has been applied to the other spouse's debts, such as unpaid child support or federal tax obligations. Like the Connecticut 8379, it requires specific information about income and tax payments to determine the appropriate allocation of the refund.

The New York Mobile Home Bill of Sale form is a legal document used to transfer ownership of a mobile home from one party to another. This form is essential for ensuring that the transaction is documented and recognized for all legal purposes. Properly completing and filing this form is crucial for both the seller and the buyer to protect their rights and interests in the sale. For those seeking assistance, Templates and Guide offer valuable resources to navigate the process effectively.

Another comparable document is the IRS Form 8857, known as the Request for Innocent Spouse Relief. This form is used when one spouse seeks relief from joint tax liability due to the other spouse's actions. While the Connecticut 8379 focuses on refund allocation, Form 8857 addresses the underlying tax liability itself. Both forms require detailed information about income, tax payments, and the circumstances surrounding the tax issues to establish eligibility for relief.

The California Form 540-2EZ serves a similar purpose for residents of California. This form is used by non-obligated spouses to claim their share of a joint refund when the other spouse owes debts. Like the Connecticut 8379, it requires the submission of joint income details and tax payments. The primary difference lies in the specific state regulations and requirements that govern each form, but the fundamental goal remains the same: to secure a fair distribution of tax refunds.

Form 8379 from the state of New York also parallels the Connecticut 8379. This form allows a non-obligated spouse to claim their portion of a joint tax refund when the other spouse has outstanding debts. Both forms require similar documentation, including income and tax payment details. The New York version, however, is tailored to that state's tax laws, which can differ from Connecticut's regulations.

The Florida Department of Revenue has a form called the Application for Innocent Spouse Relief. This document is used when a spouse seeks relief from joint tax liabilities. While it is not strictly a refund claim form, it shares the same intent of protecting one spouse from the financial consequences of the other's tax obligations. Both forms require substantial documentation to support the claim, emphasizing the importance of accurate record-keeping.

The IRS Form 1040X, which is an Amended U.S. Individual Income Tax Return, can also be seen as similar in purpose. While it is not specifically designed for non-obligated spouses, it allows taxpayers to amend their returns to correct errors or adjust their tax liabilities. In situations where a spouse may have been unfairly penalized due to joint filing, a 1040X could be filed alongside the Connecticut 8379 to rectify the situation and claim any due refunds.

Additionally, the Massachusetts Form 1-NR/PY serves a similar function for non-resident and part-year resident filers. This form allows individuals to report their income accurately while also addressing issues related to joint tax refunds. Like the Connecticut 8379, it requires detailed income reporting and can help ensure that each spouse receives their rightful share of any overpayment.

The Illinois Form IL-1040-X, the Amended Individual Income Tax Return, is another comparable document. This form allows taxpayers to correct previously filed returns and claim refunds. While it is not exclusively for non-obligated spouses, it can be used in conjunction with the Connecticut 8379 to ensure that any overpayments are accurately allocated between spouses.

Finally, the Pennsylvania Form PA-40, the Pennsylvania Personal Income Tax Return, also has a similar function for married couples. This form allows spouses to file jointly and addresses any issues related to joint refunds. Like the Connecticut 8379, it requires detailed reporting of income and tax payments, ensuring that each spouse's contributions are recognized in the final tax calculations.