Free Connecticut Reg 15 PDF Template

Free Connecticut Reg 15 PDF Template

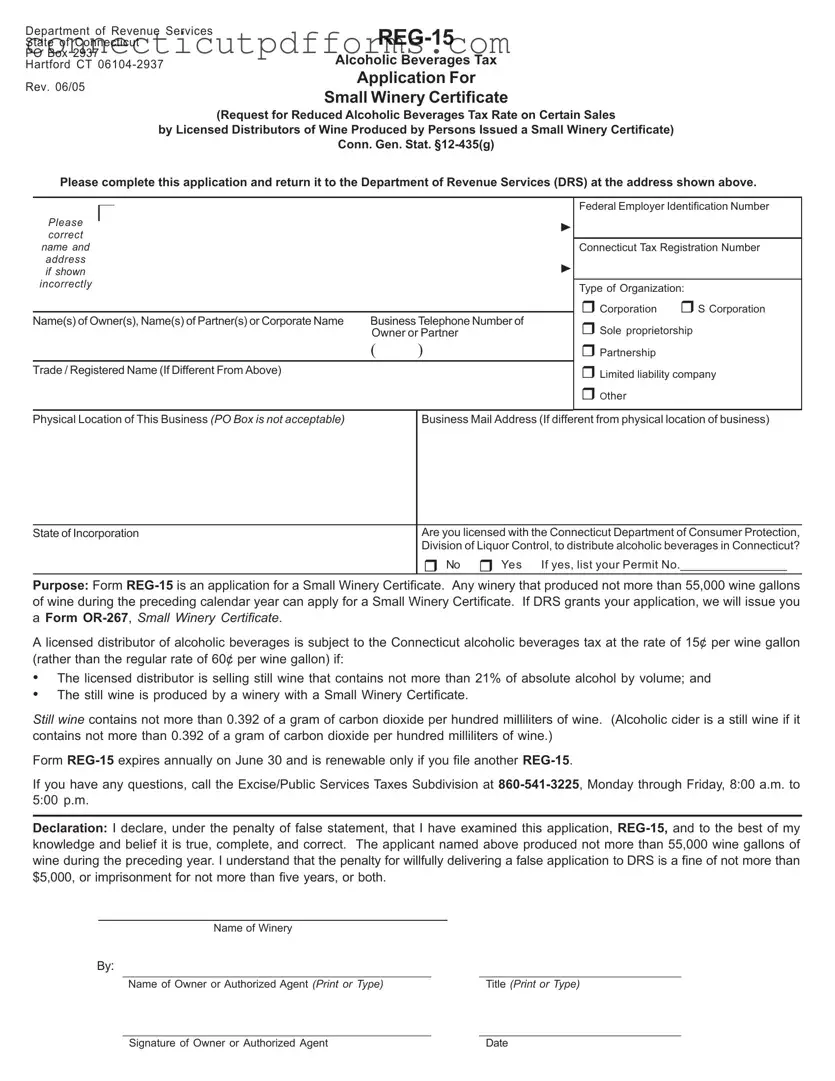

The Connecticut Reg 15 form is an essential application for wineries seeking to benefit from a reduced alcoholic beverages tax rate. Specifically designed for small wineries, this form allows those who produced no more than 55,000 wine gallons in the previous calendar year to apply for a Small Winery Certificate. By submitting the REG-15, wineries can potentially lower their tax burden from the standard rate of 60 cents per wine gallon to just 15 cents, provided they meet certain criteria. This form requires key information such as the owner's name, business address, and federal tax identification number, ensuring that all applicants are properly registered and licensed to distribute alcoholic beverages in Connecticut. Additionally, the application must be renewed annually, as it expires on June 30. For any inquiries regarding the form or the application process, the Excise/Public Services Taxes Subdivision is available to assist during regular business hours. Completing the REG-15 accurately is crucial, as any false statements can lead to significant penalties. Understanding these aspects of the Connecticut Reg 15 form can help wineries navigate the tax landscape more effectively and take advantage of the benefits available to them.

Filing for Custody - Appropriate legal documentation is vital for establishing your claims in custody or visitation cases.

For individuals looking to take action against unwelcome activities, the process of obtaining a necessary Cease and Desist Letter template can be streamlined by visiting the following resource: simple guide to the Cease and Desist Letter process.

Ct Teaching Requirements - A nonrefundable application fee of $50 must accompany the ED 170 form.

| Fact Name | Fact Description |

|---|---|

| Purpose of Form | Form REG-15 is used to apply for a Small Winery Certificate, allowing for a reduced tax rate on certain wine sales. |

| Eligibility | A winery must produce no more than 55,000 wine gallons of wine in the previous year to qualify for the certificate. |

| Tax Rate | Licensed distributors can pay a reduced tax rate of 15¢ per wine gallon instead of the standard 60¢ if they sell eligible still wine. |

| Expiration | The REG-15 form expires annually on June 30 and must be renewed by submitting a new application. |

| Governing Law | This form is governed by Conn. Gen. Stat. §12-435(g), which outlines the small winery tax provisions. |

| Contact Information | Questions can be directed to the Excise/Public Services Taxes Subdivision at 860-541-3225 during business hours. |

| False Statements Penalty | Submitting false information can result in a fine of up to $5,000 or imprisonment for up to five years, or both. |

Department of Revenue Services |

||

State of Connecticut |

||

PO Box 2937 |

Alcoholic Beverages Tax |

|

Hartford CT |

||

|

||

Rev. 06/05 |

Application For |

|

Small Winery Certificate |

||

|

(Request for Reduced Alcoholic Beverages Tax Rate on Certain Sales

by Licensed Distributors of Wine Produced by Persons Issued a Small Winery Certificate)

Conn. Gen. Stat.

Please complete this application and return it to the Department of Revenue Services (DRS) at the address shown above.

Please correct name and address if shown incorrectly

Name(s) of Owner(s), Name(s) of Partner(s) or Corporate Name |

Business Telephone Number of |

|

|

Owner or Partner |

|

|

( |

) |

Trade / Registered Name (If Different From Above)

Federal Employer Identification Number

Connecticut Tax Registration Number

Type of Organization:

Corporation |

S Corporation |

Sole proprietorship

Partnership

Limited liability company

Other

Physical Location of This Business (PO Box is not acceptable)

Business Mail Address (If different from physical location of business)

State of Incorporation

Are you licensed with the Connecticut Department of Consumer Protection, Division of Liquor Control, to distribute alcoholic beverages in Connecticut?

No |

Yes If yes, list your Permit No._________________ |

Purpose: Form

aForm

A licensed distributor of alcoholic beverages is subject to the Connecticut alcoholic beverages tax at the rate of 15¢ per wine gallon (rather than the regular rate of 60¢ per wine gallon) if:

•The licensed distributor is selling still wine that contains not more than 21% of absolute alcohol by volume; and

•The still wine is produced by a winery with a Small Winery Certificate.

Still wine contains not more than 0.392 of a gram of carbon dioxide per hundred milliliters of wine. (Alcoholic cider is a still wine if it contains not more than 0.392 of a gram of carbon dioxide per hundred milliliters of wine.)

Form

If you have any questions, call the Excise/Public Services Taxes Subdivision at

Declaration: I declare, under the penalty of false statement, that I have examined this application,

Name of Winery

By: __________________________________________________________ |

______________________________________ |

Name of Owner or Authorized Agent (Print or Type) |

Title (Print or Type) |

__________________________________________________________ |

______________________________________ |

Signature of Owner or Authorized Agent |

Date |

Completing the Connecticut Reg 15 form can seem straightforward, but many applicants stumble on key details. One common mistake is failing to provide accurate contact information. The form requests the business telephone number, and leaving this blank can lead to delays in processing. Always double-check that the number is correct and clearly written.

Another frequent error is neglecting to specify the physical location of the business. A PO Box is not acceptable. Applicants often mistakenly believe that a mailing address suffices. This can result in the application being rejected outright. Ensure that the physical address is complete and accurate, as this is crucial for compliance.

Many applicants also overlook the requirement to indicate their type of organization. Whether it’s a corporation, partnership, or sole proprietorship, selecting the correct option is essential. Failure to do so can lead to confusion and complications during the review process.

In addition, some individuals forget to check their licensing status with the Connecticut Department of Consumer Protection. The form asks whether you are licensed to distribute alcoholic beverages in Connecticut. If you answer "yes," it’s vital to provide your permit number. Omitting this detail can hinder your application’s progress.

Another mistake relates to the declaration section. Some applicants fail to sign or date the form. This might seem minor, but without a signature, the application is incomplete. It’s a simple step that can prevent unnecessary delays.

Additionally, many people misinterpret the production limits. The form specifies that only wineries producing not more than 55,000 wine gallons of wine during the preceding year can apply. Misunderstanding this requirement can lead to ineligibility. Be sure to verify your production figures before submitting the application.

Applicants sometimes forget to renew their application annually. The REG-15 form expires on June 30 each year, and failing to file a new application can result in losing the reduced tax rate. Set a reminder to ensure you stay compliant and maintain your benefits.

Lastly, be cautious about the accuracy of your declaration. Misrepresenting information, even unintentionally, can lead to severe penalties. Familiarize yourself with the implications of false statements and take the time to review your application thoroughly. Accuracy is not just important; it is essential.

When filling out the Connecticut Reg 15 form, there are several important aspects to consider. Understanding these key points can help ensure a smooth application process for a Small Winery Certificate.

Completing the REG-15 form accurately and understanding its implications can lead to valuable tax savings and compliance with state regulations. Take your time to ensure everything is correct before submission.

The Connecticut Reg 15 form is similar to the IRS Form 1065, which is used for partnerships to report income, deductions, and other tax-related information. Both forms require detailed information about the business structure and ownership. Just as the Reg 15 focuses on wineries and their production levels, Form 1065 emphasizes the partnership's financial performance. Each document serves to establish eligibility for specific tax benefits, ensuring that the entities comply with their respective regulatory bodies.

Another document comparable to the Connecticut Reg 15 is the IRS Form 990, which non-profit organizations use to report their financial activities. Like the Reg 15, Form 990 requires organizations to disclose their operational details, including income sources and expenses. Both forms aim to promote transparency and accountability, allowing regulatory agencies to assess compliance with tax obligations. While Reg 15 targets small wineries, Form 990 addresses a broader range of non-profit entities.

The Connecticut Business Entity Tax Registration Form is also similar to the Reg 15. This form is essential for businesses operating in Connecticut to register for state taxes. Both documents require information about the business structure, ownership, and contact details. They serve as foundational paperwork for establishing a business's tax obligations. Just as the Reg 15 provides a pathway for wineries to access reduced tax rates, the Business Entity Tax Registration Form ensures that all businesses are recognized for tax purposes.

Form ST-5, the Connecticut Exempt Use Certificate, shares similarities with the Reg 15 as it relates to tax exemptions. This form is used by purchasers to claim exemption from sales tax on specific items. Both forms require detailed information about the entity and its operations. They help ensure that tax benefits are appropriately applied, allowing qualified entities to operate under reduced tax burdens. The focus remains on compliance and proper documentation to avoid penalties.

The Connecticut Sales and Use Tax Resale Certificate is another document that parallels the Reg 15. This certificate allows businesses to purchase goods without paying sales tax if those goods are intended for resale. Both documents aim to facilitate tax compliance while providing financial benefits to eligible entities. Each requires clear identification of the business and its intended use of the products, ensuring that tax exemptions are correctly applied.

Form CT-1040, the Connecticut Resident Income Tax Return, is also relevant. It is used by individuals to report their income and calculate their state tax liability. Like the Reg 15, it requires detailed personal and financial information. Both forms are designed to ensure that taxpayers meet their obligations while providing opportunities for potential tax reductions. The focus is on compliance with state tax laws, albeit for different types of taxpayers.

Another comparable document is the Connecticut Corporation Business Tax Return (Form CT-1120). This form is used by corporations to report their income and calculate their business taxes. Similar to the Reg 15, it requires detailed financial information and is essential for ensuring compliance with state tax regulations. Both forms provide avenues for potential tax benefits, reflecting the importance of proper documentation and reporting in the business landscape.

When engaging in the sale of a boat, it's crucial to have the appropriate documentation in place, such as the nyforms.com/boat-bill-of-sale-template/, which outlines the terms of the sale and formalizes the transfer of ownership between the seller and buyer. This not only provides legal protection but also ensures that both parties are in agreement regarding the details of the transaction.

The Connecticut Partnership Tax Return (Form CT-1065) is similar as well. This form is specifically designed for partnerships to report income and deductions. Like the Reg 15, it requires detailed information about the partnership structure and financial performance. Both forms aim to ensure that entities comply with tax laws while providing opportunities for tax benefits. They emphasize the importance of accurate reporting in maintaining good standing with state authorities.

Lastly, the Connecticut Employer Tax Registration Form is relevant to the discussion. This form is used by employers to register for state payroll taxes. Like the Reg 15, it requires essential information about the business and its operations. Both documents serve as critical components in the tax compliance framework, ensuring that businesses meet their obligations while potentially accessing benefits. They highlight the necessity of proper registration and documentation in the business environment.