Free Connecticut Sba 2 PDF Template

Free Connecticut Sba 2 PDF Template

The Connecticut SBA 2 form serves a crucial role for individuals holding a Certified Public Accountant (CPA) Certificate who wish to register their certification in the state. This registration allows them to use the title "Certified Public Accountant" and the initials "CPA" under specific circumstances. Applicants must complete the form accurately, providing their name, contact information, and CPA certificate number, along with the issuing jurisdiction. A fee of $40 is required, which can be paid via check, money order, cashier's check, or credit card, necessitating the submission of a separate payment sheet for the latter. The completed form must be mailed to the State Board of Accountancy, where it will be reviewed and placed on the agenda for the next board meeting, typically held monthly. It is important to note that registration does not confer the authority to practice public accountancy; rather, it permits limited use of the CPA title in personal and professional contexts. Registered certificate holders may use the title in personal correspondence, on business cards, and in communications related to their employment, provided they do not misrepresent their professional status. This form thus facilitates a pathway for CPA certificate holders to maintain their professional identity while adhering to the regulatory framework established by the Connecticut State Board of Accountancy.

Connecticut Fpd 124 - Using the form correctly prevents misunderstandings with local law enforcement.

Ed 186 - All requested documents must be attached to avoid processing issues.

Having a well-prepared Bill of Sale form is crucial for any transaction, as it ensures that both parties are aware of the agreement and its terms. For those in New York, utilizing a reliable template can streamline the process and provide all necessary details. For more information and to access a convenient template, visit https://nyforms.com/bill-of-sale-template.

Filing for Custody - This form is used to apply for custody or visitation rights in Connecticut.

| Fact Name | Description |

|---|---|

| Form Purpose | This form is used to register a CPA Certificate in Connecticut, allowing limited use of the title "Certified Public Accountant" and the initials "CPA". |

| Governing Law | The registration is governed by Section 20-280-20 of the Connecticut State Board of Accountancy Regulations. |

| Application Fee | A payment of $40.00 is required, payable by check, money order, or cashier’s check to the Treasurer of the State of Connecticut. |

| Submission Instructions | Completed forms must be mailed to the State Board of Accountancy, Payment Center, at the specified address. |

| Validity Period | The registration is valid for the remainder of the calendar year in which it is granted, from January 1 to December 31. |

| Limitations on Use | Registration does not grant authority to practice public accountancy. Certain restrictions apply to the use of the title "CPA". |

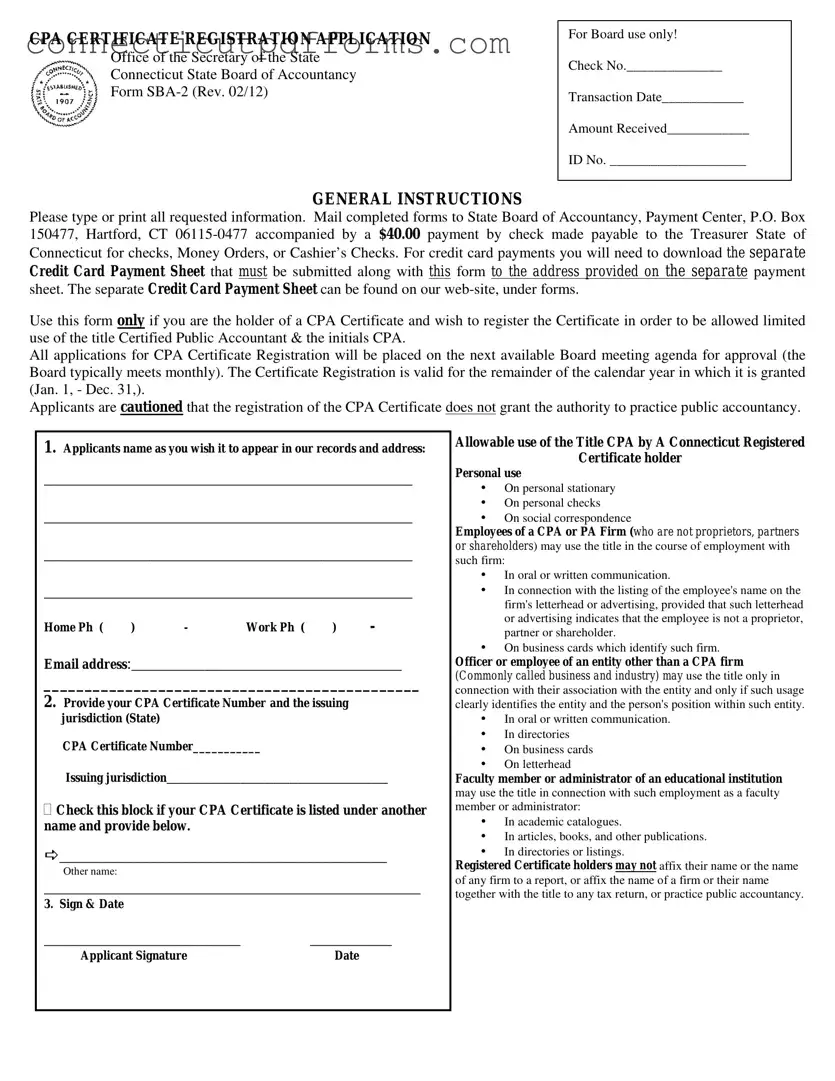

CPA CERTIFICATE REGISTRATION APPLICATION

Office of the Secretary of the State

Connecticut State Board of Accountancy

Form

For Board use only!

Check No.______________

Transaction Date____________

Amount Received____________

ID No. ____________________

GENERAL INSTRUCTIONS

Please type or print all requested information. Mail completed forms to State Board of Accountancy, Payment Center, P.O. Box 150477, Hartford, CT

Use this form only if you are the holder of a CPA Certificate and wish to register the Certificate in order to be allowed limited use of the title Certified Public Accountant & the initials CPA.

All applications for CPA Certificate Registration will be placed on the next available Board meeting agenda for approval (the Board typically meets monthly). The Certificate Registration is valid for the remainder of the calendar year in which it is granted (Jan. 1, - Dec. 31,).

Applicants are cautioned that the registration of the CPA Certificate does not grant the authority to practice public accountancy.

1.Applicants name as you wish it to appear in our records and address:

_____________________________________________

_____________________________________________

_____________________________________________

_____________________________________________

Home Ph ( ) -Work Ph ( ) -

Email address:_________________________________

______________________________________________

2.Provide your CPA Certificate Number and the issuing jurisdiction (State)

CPA Certificate Number___________

Issuing jurisdiction___________________________

Check this block if your CPA Certificate is listed under another name and provide below.

________________________________________

Other name:

______________________________________________

3. Sign & Date

________________________ |

__________ |

Applicant Signature |

Date |

Allowable use of the Title CPA by A Connecticut Registered

Certificate holder

Personal use

•On personal stationary

•On personal checks

•On social correspondence

Employees of a CPA or PA Firm (who are not proprietors, partners or shareholders) may use the title in the course of employment with such firm:

•In oral or written communication.

•In connection with the listing of the employee's name on the firm's letterhead or advertising, provided that such letterhead or advertising indicates that the employee is not a proprietor, partner or shareholder.

•On business cards which identify such firm.

Officer or employee of an entity other than a CPA firm

(Commonly called business and industry) may use the title only in connection with their association with the entity and only if such usage clearly identifies the entity and the person's position within such entity.

•In oral or written communication.

•In directories

•On business cards

•On letterhead

Faculty member or administrator of an educational institution may use the title in connection with such employment as a faculty member or administrator:

•In academic catalogues.

•In articles, books, and other publications.

•In directories or listings.

Registered Certificate holders may not affix their name or the name of any firm to a report, or affix the name of a firm or their name together with the title to any tax return, or practice public accountancy.

Section

Use of the title "Certified Public Accountant" upon registration of a certificate

(a)Definitions. As used in this section:

(1)"Certificate" means a Connecticut, "certified" public accountant" certificate issued either prior to October 1, 1992, or pursuant to section

(2)"Firm" means any person, proprietorship, partnership, corporation or association and any other legal entity that practices public accountancy;

(3)"License" means a public accountancy license issued pursuant to section

(4)"Licensee" means the holder of a certificate issued pursuant to section

(5)"Permit,” means a permit to practice public accountancy issued to a firm pursuant to section

(6)"Practicing public accountancy" means performing for the public or offering to perform for the public for a fee by a person or firm holding himself or itself out to the public as a licensee one or more kinds of services involving the use of accounting or auditing skills, including, but not limited to, the issuance of reports on financial statements, or of one or more kinds of management advisory, financial advisory or consulting services, or the preparation of tax returns of the furnishing of advice on tax matters;

(7)"Registration" or "Registered" means, when used in the context of a certificate, registration pursuant to subsection (f) of section

(8)"Report" means any writing which refers to a financial statement and (A) expresses or implies assurance as to the reliability of said financial statement, and includes, but is not limited to, any writing disclaiming an opinion, when such writing contains language conventionally understood in the profession to express or imply assurance as to the reliability of such financial statement, and (B) expresses or implies that the person or firm issuing such writing has special competence in accounting or auditing, which expression or implication arises from, among other things, the use of written language which is conventionally understood in the profession to express or imply assurance as to the reliability of financial statements.

(9)"Title pertaining to certification" or "Title pertaining to such certification" means the title or designation "certified public accountant" or the abbreviation "CPA" or any other title, designation, words, letters, abbreviations, sign, card or device tending to indicate that a person is a certified public accountant.

(b)The holder of a certificate who does not also hold a license shall not use the title pertaining to such certification except as permitted by this section of the regulations of the Connecticut state agencies.

(c)In addition to the use permitted by subsection (g) of this section, the holder of a registered certificate who is an employee of a firm which holds a current permit to practice public accountancy but who is not a proprietor, partner or shareholder of such firm, may use the title pertaining to such certification, only in the course of his employment with such firm, in oral or written communication, in connection with the listing of such employee's name on the firm's letterhead an in advertising for the firm, provided that such letterhead or advertising indicates that such employee is not a proprietor, partner or shareholder in such firm, and in connection with the listing of such employee's name on business cards which identify such firm.

(d)In addition to the use permitted by subsection (g) of this section, the holder of a registered certificate actively employed as a faculty member or administrator of an educational institution, whether public or private, for profit or nonprofit, may use the title pertaining to such certification only in connection with such employment as a faculty member or administrator, including ,but not limited to, use in academic catalogues, articles, books and other publication and in academic directories or listings.

(e)In addition to the use permitted by subsection (g) of this section, the holder of a registered certificate who is an officer or employee of an entity other than a firm engaged in the practice of public accountancy may use the title pertaining to such certification only in connection with his association with such entity and only if such usage clearly identifies the entity and the person's position within such entity, and may include use on correspondence, business cards, directories, and oral or written communication.

(f) . Nothing in this section shall be construed to allow the holder of a certificate, who does not also hold a license, to affix his name or the name of any firm to a report, or to affix the name of a firm or his name together with the title pertaining to such certification to any tax return, or to allow the holder of a certificate, who does not also hold a license and a permit, to practice public accountancy

(g)The holder of a certificate may use the title pertaining to such certification on personal stationary, checks and social correspondence, provided that, except as provided in subsections (c), (d) and (e) of this section, such title shall not be used in connection with any activity engaged in for the purpose of generating income or which does generate income.

Filling out the Connecticut SBA-2 form can be a straightforward process, but many applicants make common mistakes that can lead to delays or complications. One frequent error is failing to provide complete and accurate information in the applicant's name and address section. It is crucial to ensure that the name appears exactly as desired in the records. Any discrepancies can cause issues during processing, so double-checking this information is essential.

Another common mistake involves neglecting to include the CPA Certificate Number and the issuing jurisdiction. Applicants often overlook this section, thinking it is unnecessary. However, this information is vital for verifying the applicant's credentials. Without it, the application may be considered incomplete, leading to potential rejection.

Some applicants mistakenly check the block indicating their CPA Certificate is listed under another name without providing the necessary details. If this applies, it is essential to specify the other name clearly. Omitting this information can create confusion and hinder the application process.

Signatures and dates are critical components of the application. Many individuals forget to sign or date the form, which can result in automatic rejection. It's a simple step that can easily be overlooked, but it is vital for the application to be considered valid.

Payment errors also frequently occur. Applicants must ensure that they include the correct payment amount of $40.00 and that the payment method aligns with the instructions provided. Submitting the wrong amount or using an unsupported payment method can lead to processing delays.

In addition, some applicants fail to follow the specific instructions regarding credit card payments. If opting for this method, it is necessary to download the separate Credit Card Payment Sheet and submit it alongside the SBA-2 form. Ignoring this requirement can result in a delay in processing the application.

Lastly, many applicants do not take the time to review the allowable use of the title "Certified Public Accountant." Understanding these regulations is essential to avoid misusing the title and facing potential penalties. Familiarizing oneself with the guidelines ensures compliance and helps maintain professional integrity.

When filling out and using the Connecticut SBA-2 form, keep these key takeaways in mind:

The Connecticut SBA 2 form is similar to the CPA License Application, which is a document used by individuals seeking to obtain a license to practice as a Certified Public Accountant. Both forms require applicants to provide personal information, including their name and contact details, and they typically involve a fee for processing. However, while the SBA 2 form is specifically for registering an existing CPA certificate for limited use of the title, the CPA License Application is the initial step for those who have not yet been certified. The CPA License Application may also include additional requirements such as proof of education and examination results.

A New York Lease Agreement form serves a vital role in outlining the contractual relationship between landlords and tenants, ensuring that both parties understand their legal rights and obligations. To navigate this process effectively, one can refer to helpful resources such as Templates and Guide, which provide valuable templates and insights into creating a clear and comprehensive lease document that protects the interests of all involved.

Another document that resembles the Connecticut SBA 2 form is the CPA Renewal Application. This form is used by CPAs to renew their licenses periodically, ensuring they remain compliant with state regulations. Like the SBA 2 form, it requires personal information and often a fee. However, the renewal application focuses on maintaining an active license rather than registering a certificate. It may also require proof of continuing education to demonstrate that the CPA has kept up with industry standards and practices.

The Professional Corporation Registration form is another document that shares similarities with the Connecticut SBA 2 form. This form is used by CPAs who wish to form a professional corporation to practice accountancy. Both documents require detailed information about the individual and their qualifications. The key difference lies in the purpose: the SBA 2 form is for registration of an existing certificate, while the Professional Corporation Registration is about establishing a legal business entity for practice.

The Business Entity Registration form also has similarities to the SBA 2 form. This document is used by CPAs who want to register their business with the state. Both forms require essential information about the applicant and may involve a fee. However, the Business Entity Registration focuses on the business structure rather than the individual's qualifications. It is essential for CPAs who want to operate under a specific business model, such as a partnership or corporation.

The Application for Firm Registration is another relevant document. This form is used by CPA firms to register their business with the state board. Like the SBA 2 form, it requires details about the firm and its owners. However, the focus is on the firm’s qualifications and compliance with state regulations rather than the individual CPA's certification. Both forms are crucial for ensuring that the respective parties are recognized and authorized to operate within Connecticut.

The Continuing Professional Education (CPE) Reporting form is similar in that it requires CPAs to report their completed education hours. While the SBA 2 form registers a CPA certificate for limited use, the CPE Reporting form ensures that CPAs maintain their knowledge and skills through ongoing education. Both forms serve to uphold standards within the profession, but they target different aspects of a CPA's career—registration versus education compliance.

Lastly, the Application for Reinstatement of a CPA License is another document that bears resemblance to the Connecticut SBA 2 form. This application is for CPAs who have let their licenses lapse and wish to reinstate them. Both forms require personal details and may involve fees. However, the reinstatement application focuses on returning to active practice, while the SBA 2 form is about registering an existing certificate for limited title use. Each document plays a vital role in ensuring that CPAs remain compliant with state regulations and standards.