Free Employee Quarterly Earnings Report PDF Template

Free Employee Quarterly Earnings Report PDF Template

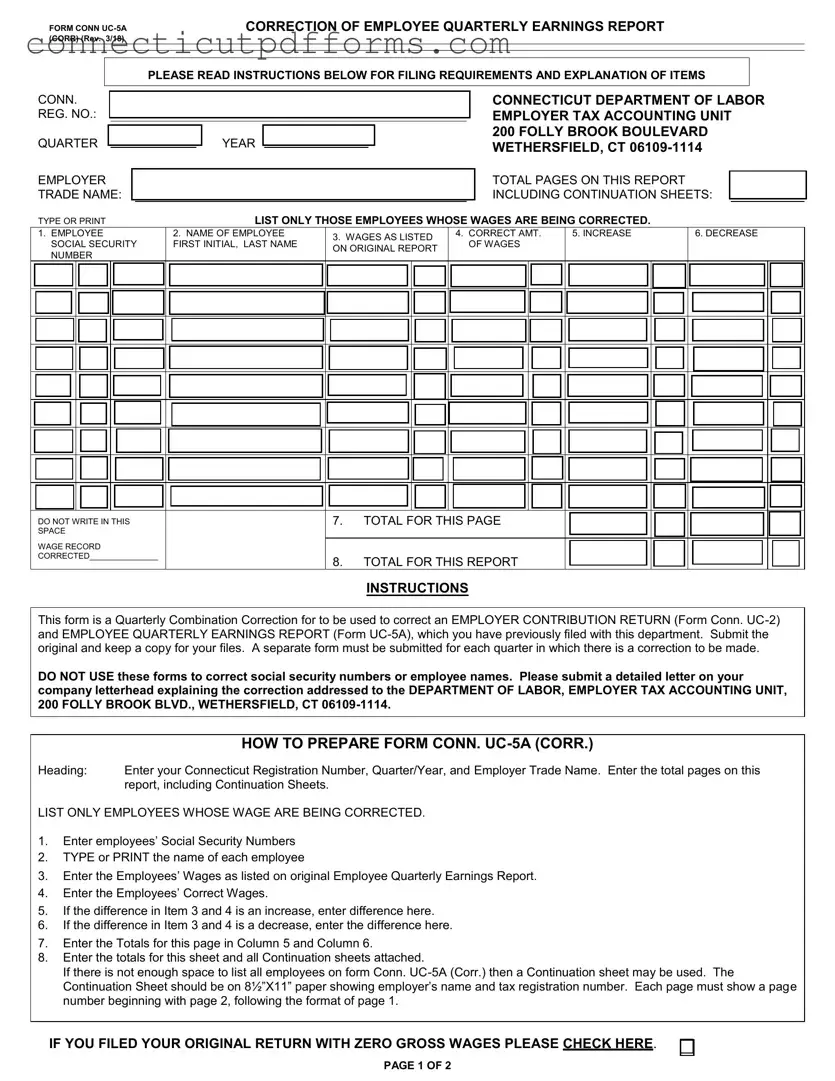

The Employee Quarterly Earnings Report form, known as Form Conn UC-5A (Corr), serves a critical function for employers in Connecticut. This form is specifically designed to correct any inaccuracies in previously submitted Employer Contribution Returns and Employee Quarterly Earnings Reports. Employers must submit this correction form when adjustments to employee wages are necessary. It is important to note that this form should only list employees whose wages are being corrected, and it requires detailed information such as Social Security numbers, original wages, and corrected wages. Additionally, the form mandates that employers provide a letter explaining the corrections, which must be addressed to the Department of Labor's Employer Tax Accounting Unit. Each quarter requiring corrections necessitates a separate submission of this form, ensuring clarity and accuracy in reporting. Employers must also be aware that this form is not intended for correcting employee names or Social Security numbers. By following the specified instructions, including the use of continuation sheets if needed, employers can effectively navigate the correction process, thereby maintaining compliance with state regulations.

Connecticut Sba 2 - Identify your CPA certificate number and issuing jurisdiction on the form.

For those seeking to draft their own document, resources such as Templates and Guide can provide valuable assistance in ensuring that the agreement meets all necessary legal standards and covers all essential aspects of the LLC's operations.

Connecticut Capital Improvement - Note who was awarded the contract based on the bids.

| Fact Name | Details |

|---|---|

| Form Title | Correction of Employee Quarterly Earnings Report (Form Conn. UC-5A) |

| Governing Law | Connecticut General Statutes, Title 31, Chapter 567 |

| Submission Requirements | Submit the original form and retain a copy for your records. |

| Employee Listing | Only list employees whose wages are being corrected on the form. |

| Correction Process | A separate form must be submitted for each quarter requiring a correction. |

| Additional Documentation | A detailed letter on company letterhead must accompany the form, explaining the corrections. |

FORM CONN

CORRECTION OF EMPLOYEE QUARTERLY EARNINGS REPORT

PLEASE READ INSTRUCTIONS BELOW FOR FILING REQUIREMENTS AND EXPLANATION OF ITEMS

CONN.

REG. NO.:

QUARTER

EMPLOYER TRADE NAME:

YEAR

CONNECTICUT DEPARTMENT OF LABOR EMPLOYER TAX ACCOUNTING UNIT 200 FOLLY BROOK BOULEVARD WETHERSFIELD, CT

TOTAL PAGES ON THIS REPORT INCLUDING CONTINUATION SHEETS:

TYPE OR PRINT |

LIST ONLY THOSE EMPLOYEES WHOSE WAGES ARE BEING CORRECTED. |

1.EMPLOYEE SOCIAL SECURITY NUMBER

2.NAME OF EMPLOYEE

FIRST INITIAL, LAST NAME

3.WAGES AS LISTED ON ORIGINAL REPORT

4.CORRECT AMT. OF WAGES

5. INCREASE

6. DECREASE

DO NOT WRITE IN THIS SPACE

WAGE RECORD

CORRECTED_______________

7.TOTAL FOR THIS PAGE

8.TOTAL FOR THIS REPORT

INSTRUCTIONS

This form is a Quarterly Combination Correction for to be used to correct an EMPLOYER CONTRIBUTION RETURN (Form Conn.

DO NOT USE these forms to correct social security numbers or employee names. Please submit a detailed letter on your company letterhead explaining the correction addressed to the DEPARTMENT OF LABOR, EMPLOYER TAX ACCOUNTING UNIT, 200 FOLLY BROOK BLVD., WETHERSFIELD, CT

|

HOW TO PREPARE FORM CONN. |

Heading: |

Enter your Connecticut Registration Number, Quarter/Year, and Employer Trade Name. Enter the total pages on this |

|

report, including Continuation Sheets. |

LIST ONLY EMPLOYEES WHOSE WAGE ARE BEING CORRECTED.

1.Enter employees’ Social Security Numbers

2.TYPE or PRINT the name of each employee

3.Enter the Employees’ Wages as listed on original Employee Quarterly Earnings Report.

4.Enter the Employees’ Correct Wages.

5.If the difference in Item 3 and 4 is an increase, enter difference here.

6.If the difference in Item 3 and 4 is a decrease, enter the difference here.

7.Enter the Totals for this page in Column 5 and Column 6.

8.Enter the totals for this sheet and all Continuation sheets attached.

If there is not enough space to list all employees on form Conn.

Continuation Sheet should be on 8½”X11” paper showing employer’s name and tax registration number. Each page must show a page number beginning with page 2, following the format of page 1.

IF YOU FILED YOUR ORIGINAL RETURN WITH ZERO GROSS WAGES PLEASE CHECK HERE.

PAGE 1 OF 2

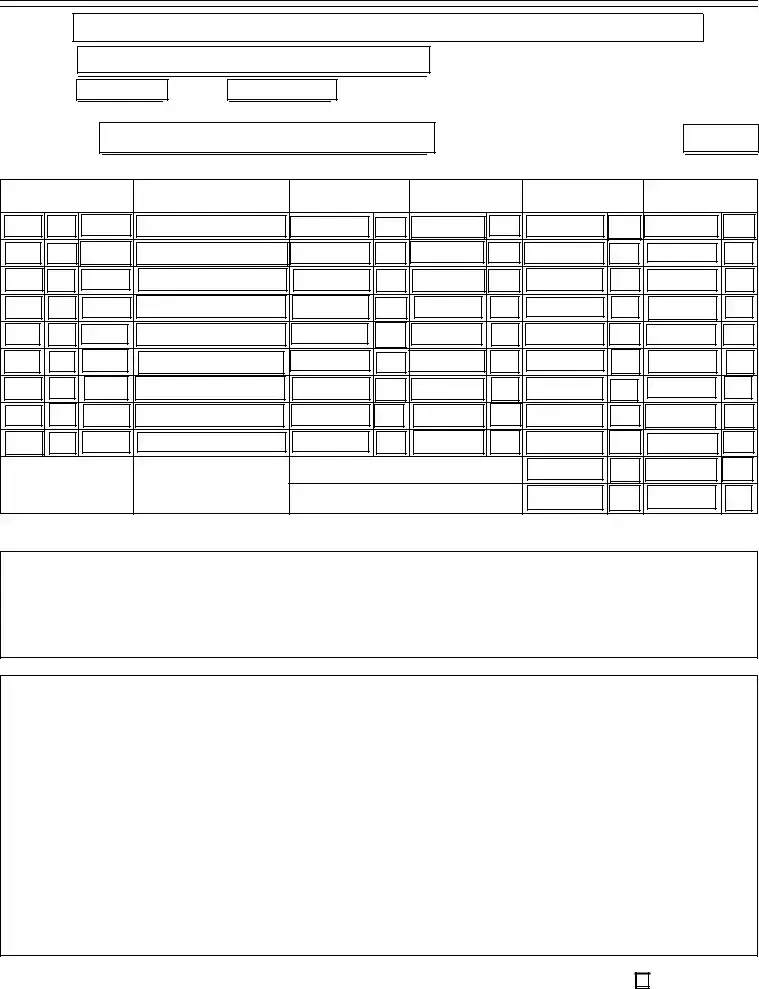

FORM CONN.

CORRECTION OF

EMPLOYER CONTRIBUTION RETURN

PLEASE COMPLETE BOTH PAGES OF THIS RETURN

QUARTER |

|

|

|

YEAR |

|

|

|

|

|

CONN. REG. NO.:

CORPORATE NAME OR

TRADE NAME

CONNECTICUT DEPARTMENT OF LABOR EMPLOYER TAX ACCOUNTING UNIT 200 FOLLY BROOK BOULEVARD WETHERSFIELD, CT

Pay Online at: www.ct.gov/doltax

ADDRESS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

COLUMN A |

|

COLUMN B |

COLUMN C |

|

COLUMN D |

|||||

|

|

|

|

|

ORIGINAL |

|

CORRECTED |

INCREASE |

|

DECREASE |

|||||

1 |

CONTRIBUTION RATE |

% |

|

RETURN |

|

RETURN |

(Difference between Column |

|

(Difference between Column |

||||||

|

|

|

|

|

|

|

|||||||||

|

See original return filed for contribution rate. |

|

(Enter below amounts |

|

|

|

A and Column B when |

|

A and Column B, when |

||||||

|

|

reported on original return for |

|

|

|

Column B is larger) |

|

Column B is smaller) |

|||||||

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

corresponding items) |

|

|

|

|

|

|

|

|

|

|

2 |

TOTAL GROSS WAGES PAID TO ALL EMPLOYEES FOR WORK |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

||||

PERFORMED IN CONNECTICUT THIS QTR |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

TOTAL GROSS WAGES PAID DURING THIS QUARTER TO EACH |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

||||

EMPLOYEE IN EXCESS OF THE LIMITATION FOR THE |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

CALENDAR YEAR |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

4 |

TOTAL TAXABLE |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

||||

DIFFERENCE BETWEEN COL. A AND B IN COL. C OR D. |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

CONTRIBUTION OR CREDIT DUE: SEE INSTRUCTIONS BELOW. |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

INTEREST DUE. IF CORRECTION RESULTED IN AN INCREASE IN CONTRIBUTION (LINE 5, COLUMN C), ENTER INTEREST |

|

|

|

********** |

|

|||||||||

|

|

|

|

||||||||||||

DUE IN COLUMN C. SEE INSTRUCTIONS BELOW. |

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

IF INCREASE IN CONTRIBUTIONS DUE (ITEM 5C), ENTER PENALTY DUE, IF ANY, IN COLUMN C. SEE INSTRUCTIONS |

|

|

|

********** |

|

|||||||||

|

|

|

|

||||||||||||

BELOW. |

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

TOTAL ADDITIONAL AMOUNT DUE – SUM OF ITEMS 5C, 6C AND 7C. PAY ONLINE AT: WWW.CT.GOV/DOLTAX |

|

|

|

********** |

|

|||||||||

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9EXPLAIN REASON FOR CORRECTION

PHONE NUMBER (

)

TITLE

DATE

HOW TO PREPARE FORM CONN.

HEADING: Enter QUARTER/YEAR, Connecticut Registration Number, Employer Trade Name, Name of Owners, Partners, or Corporate name (if other than trade name) and your Mailing address

Item 1: Contribution Rate – enter Contribution Rate for this quarter. If Rate has been corrected, use Corrected Rate.

Item 2: Enter Column “A” the Gross Wages Listed on the Original Return. Enter in Column “B” the correct amount of Gross Wages. If

Column “B” is larger than Column “A”, enter the difference in Column “C”. If Column “B” is smaller than Column “A”, enter the difference in Column “D”.

Item 3: Excess Wages – Wages paid during quarter in excess of the limitation for the calendar year. Enter the Column “A” excess wages as listed on original Return. Enter in Column “B” the correct amount of Excess Wages. Enter the Difference between Columns “A” and “B” in appropriate Column “C” or “D”.

Item 4:

Item 5:

Item 6:

Item 7:

Item 8: Item 9:

Item 10:

Item 2 minus Item 3

Enter in Column “A” the taxable Wages subject to contributions as listed on the Original Return.

Enter in Column “B” the correct amount of Taxable Wages subject to contributions. Enter difference between Columns “A” and “B” in the appropriate Column “C” and “D”.

Enter in Column “A” the Contributions listed on the Original Return. Enter in Column “B” the amount of Contributions due on corrected wages by multiplying Item 4B by the Contribution rate in Item 1. If Column “B” is larger than Column “A”, it represents Additional Contributions Due, and the difference should be entered in Column “C” (INCREASE). IF Column “B” is less than Column “A”, it represents an Overstatement of Contributions and the difference should be entered in Column “D”

(DECREASE). If a DECREASE, a refund may be issued, if applicable.

Enter in Column “C” the interest due on the additional contributions due. Multiply item 5C by the appropriate interest rate. One percent interest is charged for each month, or part thereof, that this return is filed late. Example: If the quarter being filed is the first quarter, the due date is April 30. Beginning May 1st , calculate 1% interest due. On June 1, 2% interest; on July 1, 3% interest; etc. If it is a second quarter return, interest begins to accrue August 1st; for a 3rd quarter return, November 1st; and for a 4th quarter return, February 1st .

Enter in Column “C” any penalty on the additional contributions due. A penalty of ten percent (10%) or fifty dollars ($50), whichever is greater, is assessed if the balance of contributions due is not paid within thirty days of the due date. Penalty dates: 1st quarter

Enter the total Amount due (the Sum of Items “5C”, “6C” and “7C”). Pay online at: www.ct.gov/doltax

Explain the reason for Correction fully. If additional space is required, attach a letter furnishing all facts and refer to the letter in this space.

This correction return must be signed by a responsible and duly authorized person and mailed to the address listed above. Any payment due, however, must be made online at www.ct.gov/doltax.

Filling out the Employee Quarterly Earnings Report form can be a straightforward task, but there are common mistakes that can lead to complications. Understanding these pitfalls can help ensure that your submission is accurate and complete. One major error is failing to list only the employees whose wages are being corrected. The instructions specify that only those employees with wage adjustments should be included. Including others can confuse the review process and delay corrections.

Another frequent mistake involves incorrect entry of Social Security Numbers. It is crucial to double-check these numbers, as even a single digit error can lead to significant issues. If the Social Security Number does not match the records, the correction may not be processed. Similarly, many people overlook the requirement to type or print the names of employees clearly. Illegible handwriting can result in misidentification, which complicates the correction process.

Some individuals mistakenly enter the wrong wage amounts in the original and corrected wage fields. It’s essential to accurately reflect the wages as they were reported initially and the corrected amounts. A simple transposition of numbers can lead to incorrect calculations and further complications. Additionally, when entering the differences between the original and corrected wages, some people forget to specify whether the change is an increase or a decrease. This step is vital for accurate reporting and for understanding the financial implications of the corrections.

Another common oversight is failing to total the amounts correctly. After entering all the data, it’s important to sum the totals for both the original and corrected wages. A miscalculation here can lead to discrepancies that may require further investigation. Furthermore, not using a continuation sheet when necessary can be a mistake. If there are too many employees to fit on the form, a continuation sheet should be used to ensure all relevant information is included.

Some individuals also neglect to follow the proper format for the continuation sheet. It should be on 8.5”x11” paper and clearly show the employer’s name and tax registration number. Each page must be numbered correctly, starting from page 2. Lastly, failing to submit a detailed letter explaining the corrections can lead to confusion. This letter should be on company letterhead and sent to the appropriate department, as outlined in the instructions. Taking the time to avoid these mistakes can streamline the correction process and ensure compliance with the necessary regulations.

Filling out the Employee Quarterly Earnings Report form correctly is crucial for maintaining accurate employee records and ensuring compliance with state regulations. Here are some key takeaways to keep in mind:

By keeping these points in mind, you can navigate the process of submitting corrections with greater ease and accuracy.

The Employee Quarterly Earnings Report form is similar to the W-2 form, which is used by employers to report wages paid to employees and the taxes withheld. Both documents provide crucial information about an employee's earnings for a specific period. While the Employee Quarterly Earnings Report focuses on quarterly earnings and corrections, the W-2 is an annual summary that includes year-to-date figures. Employers must submit both forms to the respective government agencies to ensure accurate reporting and compliance with tax laws.

Another comparable document is the 1099-MISC form, which reports payments made to independent contractors or freelancers. Like the Employee Quarterly Earnings Report, the 1099-MISC captures earnings for a specific timeframe. However, it differs in that it is typically used for non-employee compensation. Both forms require accurate reporting of earnings to ensure proper tax treatment and compliance with IRS regulations.

The California Boat Bill of Sale form is a crucial document used to officially record the sale and transfer of ownership of a boat in California. This form provides essential details about the vessel, the buyer, and the seller, ensuring a clear and legal transaction. Proper completion of this form helps protect the interests of both parties and facilitates a smooth transfer of ownership. For those looking to draft this important document, you can access a template through this Boat Bill of Sale form.

The Employer Contribution Return (Form UC-2) is also similar, as it is used to report contributions based on employee wages. This form details the employer’s contributions to unemployment insurance, paralleling the Employee Quarterly Earnings Report's focus on employee wages. Both forms require precise calculations and corrections when necessary, ensuring that the employer meets their obligations under state law.

The Payroll Summary Report serves a similar function by providing a comprehensive overview of all payroll transactions within a specific period. This document aggregates data on employee wages, taxes withheld, and deductions. While the Employee Quarterly Earnings Report is specific to quarterly corrections, the Payroll Summary Report offers a broader snapshot of payroll activity, making it a vital tool for employers in managing their payroll processes.

Lastly, the IRS Form 941 is comparable, as it is used to report employment taxes, including income tax withheld and Social Security and Medicare taxes. Both forms share the goal of ensuring that accurate information is reported to the government regarding employee earnings and taxes. However, Form 941 is filed quarterly and focuses on tax liabilities, while the Employee Quarterly Earnings Report emphasizes wage corrections for individual employees.