Fillable Promissory Note Form for Connecticut

Fillable Promissory Note Form for Connecticut

In Connecticut, a promissory note serves as a vital financial instrument that outlines the terms of a loan agreement between a borrower and a lender. This written document details the amount borrowed, the interest rate, and the repayment schedule, providing clarity and security for both parties involved. Essential elements of the Connecticut Promissory Note include the names and addresses of the borrower and lender, the principal amount, and the date of the loan. Additionally, it specifies the consequences of default, ensuring that all parties understand their rights and obligations. By incorporating these key components, the form not only facilitates a smooth lending process but also helps prevent potential disputes down the line. Understanding the nuances of this form can empower individuals to make informed financial decisions while fostering trust in their lending relationships.

Connecticut Warranty Deed - This document can assist in resolving any disputes related to property boundaries.

To effectively navigate the sale of a motorcycle in New York, it's essential to utilize the New York Motorcycle Bill of Sale form, which ensures clarity and legal protection for both parties involved. By understanding the importance of this document, buyers and sellers can avoid potential disputes and misunderstandings. For comprehensive resources on this topic, refer to Templates and Guide to streamline the process and ensure compliance with state regulations.

Connecticut Warranty Deed - A Quitclaim Deed can help expeditiously rectify boundary issues between neighboring properties.

| Fact Name | Details |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated party at a future date. |

| Governing Law | The Connecticut Uniform Commercial Code (UCC) governs promissory notes in Connecticut. |

| Requirements | The note must include the amount owed, the due date, and the names of the parties involved. |

| Interest Rate | Interest can be included in the note. If not specified, Connecticut law allows for a default interest rate of 10% per annum. |

| Signature | The note must be signed by the maker, who is the person promising to pay. |

| Transferability | Promissory notes in Connecticut can be transferred to another party, making them negotiable instruments. |

| Default Consequences | If the maker defaults, the payee may pursue legal action to recover the owed amount. |

| Statute of Limitations | In Connecticut, the statute of limitations for enforcing a promissory note is six years from the date of default. |

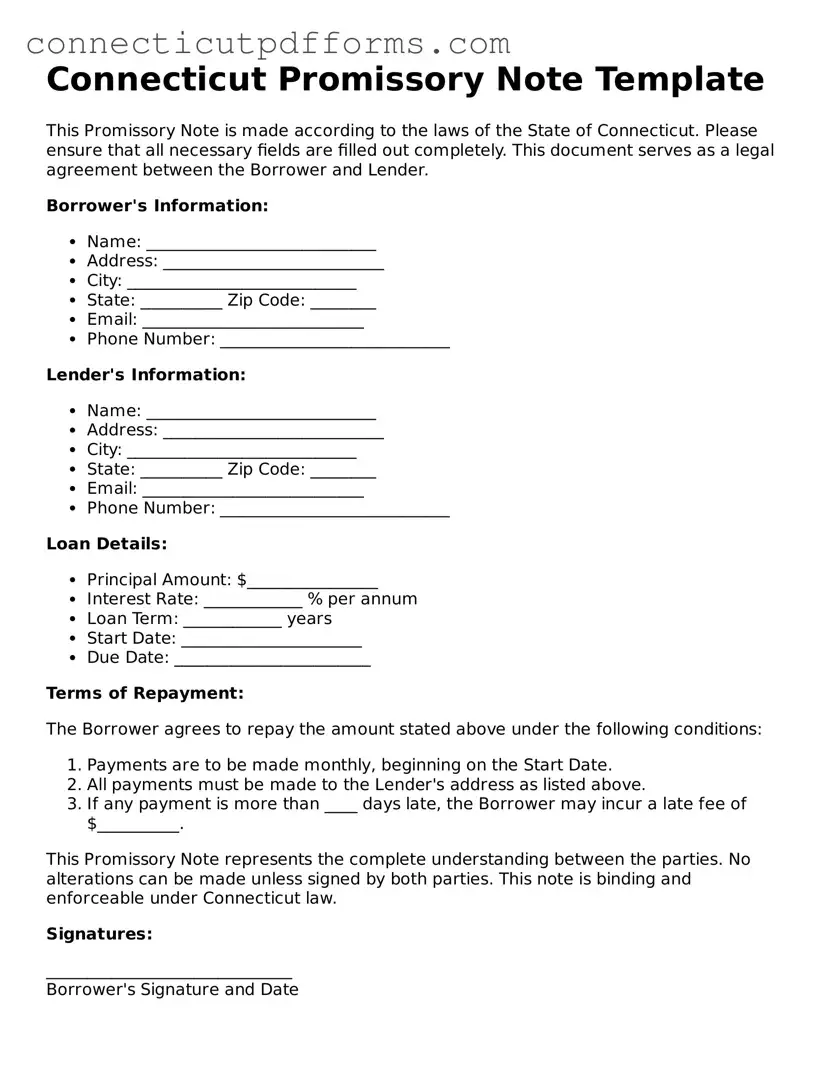

Connecticut Promissory Note Template

This Promissory Note is made according to the laws of the State of Connecticut. Please ensure that all necessary fields are filled out completely. This document serves as a legal agreement between the Borrower and Lender.

Borrower's Information:

Lender's Information:

Loan Details:

Terms of Repayment:

The Borrower agrees to repay the amount stated above under the following conditions:

This Promissory Note represents the complete understanding between the parties. No alterations can be made unless signed by both parties. This note is binding and enforceable under Connecticut law.

Signatures:

______________________________

Borrower's Signature and Date

______________________________

Lender's Signature and Date

When filling out the Connecticut Promissory Note form, many people overlook important details. One common mistake is not including the correct date. The date is crucial because it marks when the agreement takes effect. If you forget to write it down or write it incorrectly, it can lead to confusion later on.

Another frequent error is failing to clearly state the amount being borrowed. This should be written in both numbers and words. If the numbers don’t match the written amount, it can create disputes. Clarity is key here. Always double-check that both formats reflect the same value.

People often neglect to specify the interest rate. If you’re charging interest, it’s essential to include this information. Without it, the agreement may be considered incomplete. This can result in misunderstandings about how much the borrower will owe over time.

Additionally, some individuals forget to include payment terms. This includes how often payments are due and the method of payment. Whether it’s monthly, quarterly, or a lump sum, being specific helps avoid future conflicts. Make sure to outline these details clearly.

Another mistake is not signing the document. A promissory note is not valid without the signatures of both parties involved. This is a crucial step that some may overlook, thinking verbal agreements are enough. Always ensure that both parties sign and date the note.

People sometimes fail to provide a witness or notary signature. While not always required, having a witness can add an extra layer of protection. It helps verify that both parties agreed to the terms. If possible, consider having a notary public witness the signing.

Lastly, many forget to keep a copy of the signed note. Once the agreement is finalized, it’s important to retain a copy for your records. This ensures that both parties have access to the same information. Without a copy, you may find it difficult to reference the terms in the future.

When utilizing the Connecticut Promissory Note form, several key points should be considered to ensure proper completion and usage. Below are important takeaways regarding this legal document.

A loan agreement is a document that outlines the terms and conditions of a loan between a borrower and a lender. Like a promissory note, it specifies the amount borrowed, the interest rate, repayment schedule, and any collateral involved. Both documents serve to protect the lender's interests while clearly stating the obligations of the borrower. However, a loan agreement often includes additional clauses related to default and remedies, providing a more comprehensive framework for the lending relationship.

A mortgage is a legal document that secures a loan by placing a lien on real property. Similar to a promissory note, it details the amount borrowed and repayment terms. However, the mortgage also outlines the lender's rights in the event of default, allowing them to take possession of the property. While a promissory note represents the borrower's promise to repay the loan, the mortgage secures that promise with the property itself.

A secured note is akin to a promissory note but includes collateral to back the loan. This means that if the borrower defaults, the lender can claim the specified asset. Both documents outline the repayment terms and interest rates, but a secured note provides additional security for the lender. This added layer of protection can make secured notes more appealing to lenders compared to unsecured promissory notes.

An unsecured note is similar to a promissory note in that it represents a borrower's promise to repay a loan. However, unlike a secured note, it does not involve collateral. This means that if the borrower defaults, the lender has no specific asset to claim. Both documents specify repayment terms and interest rates, but the risk for lenders is higher with unsecured notes, as they rely solely on the borrower's creditworthiness.

A personal guarantee is a document where an individual agrees to repay a loan if the primary borrower defaults. Similar to a promissory note, it establishes a financial obligation. However, a personal guarantee typically involves a third party, which adds an extra layer of security for the lender. While the promissory note binds the borrower, the personal guarantee binds the guarantor, increasing the likelihood of repayment.

An installment agreement allows a borrower to repay a loan in fixed installments over time. This document shares similarities with a promissory note in that it outlines the loan amount, interest rate, and repayment schedule. However, installment agreements often provide more detailed terms regarding payment methods and consequences for missed payments. Both documents serve to formalize the lending relationship, but installment agreements can offer more structure.

When creating formal documents, utilizing resources like a comprehensive Recommendation Letter guide can provide invaluable insight into crafting effective endorsements. For detailed information, visit this link.

A lease agreement is a contract between a landlord and tenant that outlines the terms of renting property. While it is not a loan document, it shares similarities with a promissory note in that it requires regular payments over a specified period. Both documents establish obligations and can include penalties for non-compliance. However, lease agreements focus on property rental rather than a loan, making them distinct in purpose.

A business loan agreement is specifically tailored for loans made to businesses. Like a promissory note, it details the loan amount, interest rate, and repayment terms. However, it often includes additional clauses addressing business-specific risks and obligations. Both documents aim to protect the lender, but business loan agreements are more complex, reflecting the unique needs of commercial transactions.

A credit agreement outlines the terms under which a lender provides credit to a borrower. Similar to a promissory note, it specifies the amount available, interest rates, and repayment terms. However, credit agreements often include provisions for future borrowing and can cover multiple transactions. Both documents aim to establish a clear understanding of the borrower's obligations, but credit agreements can be more flexible and comprehensive.

A letter of credit is a document issued by a bank guaranteeing payment to a seller on behalf of a buyer. It shares similarities with a promissory note in that it provides a promise of payment. However, a letter of credit is typically used in international trade and involves a bank acting as an intermediary. While both documents aim to ensure payment, their applications and parties involved differ significantly.