Free Uc 2 Connecticut PDF Template

Free Uc 2 Connecticut PDF Template

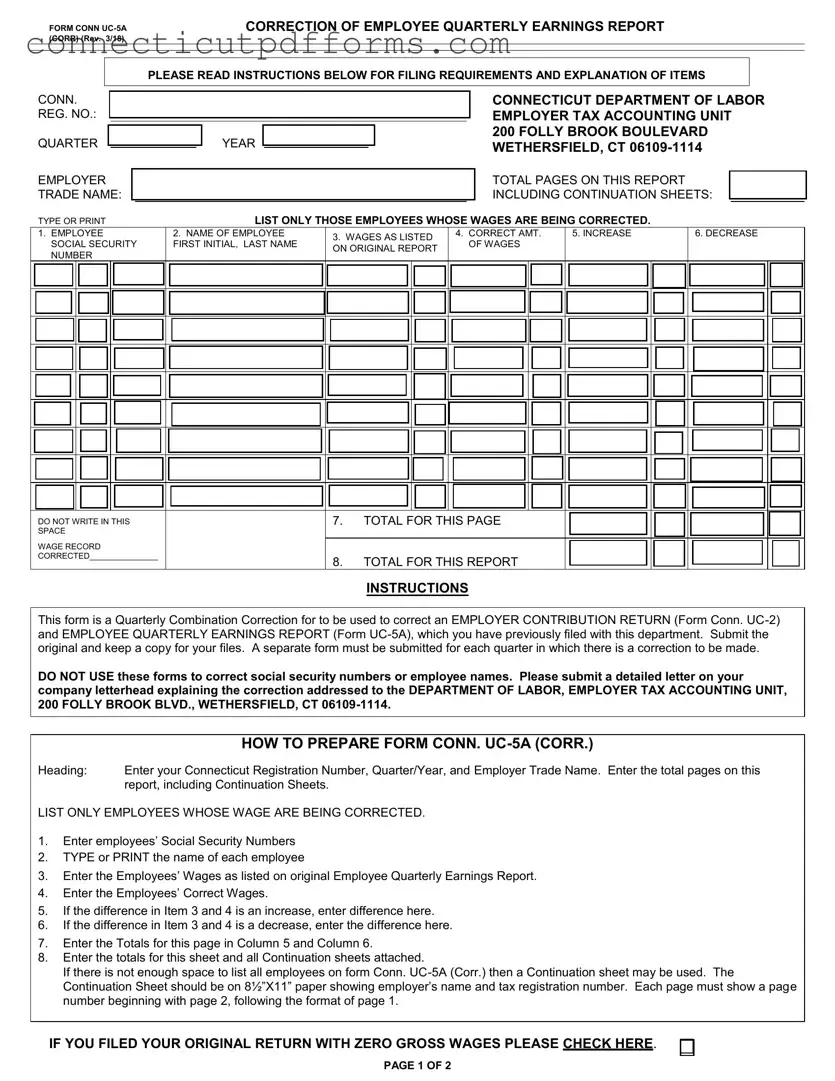

The UC-2 Connecticut form plays a crucial role in ensuring accurate reporting of employer contributions and employee earnings. This form is specifically designed for employers who need to make corrections to previously filed reports, namely the Employer Contribution Return (Form UC-2) and the Employee Quarterly Earnings Report (Form UC-5A). It is essential to submit this form for each quarter where corrections are necessary, as each quarter requires a separate submission. Employers must be careful to only list employees whose wages are being corrected, making it a focused document. Importantly, this form does not address corrections related to social security numbers or employee names; instead, a detailed letter on company letterhead must accompany such requests. The form requires various details, including the Connecticut Registration Number, the quarter and year of the report, and the employer’s trade name. Additionally, it includes specific sections for reporting gross wages, taxable wages, and contributions, allowing for a clear comparison between the original and corrected figures. Employers must also account for any penalties or interest that may apply if the corrections are filed late. By following the outlined instructions carefully, employers can ensure compliance with state regulations while maintaining accurate records of their workforce’s earnings and contributions.

Ct Dmv H13b - The bond remains valid as long as the licensee complies with legal regulations.

The New York Mobile Home Bill of Sale form is a legal document used to transfer ownership of a mobile home from one party to another. This form is essential for ensuring that the transaction is documented and recognized for all legal purposes. For those looking to obtain a professional template for this important document, you can refer to Templates and Guide, which provides valuable resources to assist both sellers and buyers in completing the sale process correctly.

Teaching Certificate Ct - The form indicates that the applicant may only serve as a substitute teacher for up to 40 days in a single assignment.

Ct Coaching Certificate - Documenting your educational journey accurately supports your commitment to coaching excellence.

| Fact Name | Description |

|---|---|

| Purpose | The UC-2 Connecticut form is used to correct previously filed employer contribution returns and employee quarterly earnings reports. |

| Governing Law | This form is governed by the Connecticut General Statutes, specifically Title 31, Chapter 567. |

| Submission Requirements | Employers must submit the original form and retain a copy for their records. A separate form is required for each quarter needing correction. |

| Employee Information | Only employees whose wages are being corrected should be listed. Do not use this form for correcting social security numbers or names. |

| Continuation Sheets | If additional space is needed, a continuation sheet may be used. It must include the employer's name and tax registration number. |

| Filing Address | Corrected forms must be mailed to the Department of Labor, Employer Tax Accounting Unit, at 200 Folly Brook Blvd, Wethersfield, CT 06109-1114. |

FORM CONN

CORRECTION OF EMPLOYEE QUARTERLY EARNINGS REPORT

PLEASE READ INSTRUCTIONS BELOW FOR FILING REQUIREMENTS AND EXPLANATION OF ITEMS

CONN.

REG. NO.:

QUARTER

EMPLOYER TRADE NAME:

YEAR

CONNECTICUT DEPARTMENT OF LABOR EMPLOYER TAX ACCOUNTING UNIT 200 FOLLY BROOK BOULEVARD WETHERSFIELD, CT

TOTAL PAGES ON THIS REPORT INCLUDING CONTINUATION SHEETS:

TYPE OR PRINT |

LIST ONLY THOSE EMPLOYEES WHOSE WAGES ARE BEING CORRECTED. |

1.EMPLOYEE SOCIAL SECURITY NUMBER

2.NAME OF EMPLOYEE

FIRST INITIAL, LAST NAME

3.WAGES AS LISTED ON ORIGINAL REPORT

4.CORRECT AMT. OF WAGES

5. INCREASE

6. DECREASE

DO NOT WRITE IN THIS SPACE

WAGE RECORD

CORRECTED_______________

7.TOTAL FOR THIS PAGE

8.TOTAL FOR THIS REPORT

INSTRUCTIONS

This form is a Quarterly Combination Correction for to be used to correct an EMPLOYER CONTRIBUTION RETURN (Form Conn.

DO NOT USE these forms to correct social security numbers or employee names. Please submit a detailed letter on your company letterhead explaining the correction addressed to the DEPARTMENT OF LABOR, EMPLOYER TAX ACCOUNTING UNIT, 200 FOLLY BROOK BLVD., WETHERSFIELD, CT

|

HOW TO PREPARE FORM CONN. |

Heading: |

Enter your Connecticut Registration Number, Quarter/Year, and Employer Trade Name. Enter the total pages on this |

|

report, including Continuation Sheets. |

LIST ONLY EMPLOYEES WHOSE WAGE ARE BEING CORRECTED.

1.Enter employees’ Social Security Numbers

2.TYPE or PRINT the name of each employee

3.Enter the Employees’ Wages as listed on original Employee Quarterly Earnings Report.

4.Enter the Employees’ Correct Wages.

5.If the difference in Item 3 and 4 is an increase, enter difference here.

6.If the difference in Item 3 and 4 is a decrease, enter the difference here.

7.Enter the Totals for this page in Column 5 and Column 6.

8.Enter the totals for this sheet and all Continuation sheets attached.

If there is not enough space to list all employees on form Conn.

Continuation Sheet should be on 8½”X11” paper showing employer’s name and tax registration number. Each page must show a page number beginning with page 2, following the format of page 1.

IF YOU FILED YOUR ORIGINAL RETURN WITH ZERO GROSS WAGES PLEASE CHECK HERE.

PAGE 1 OF 2

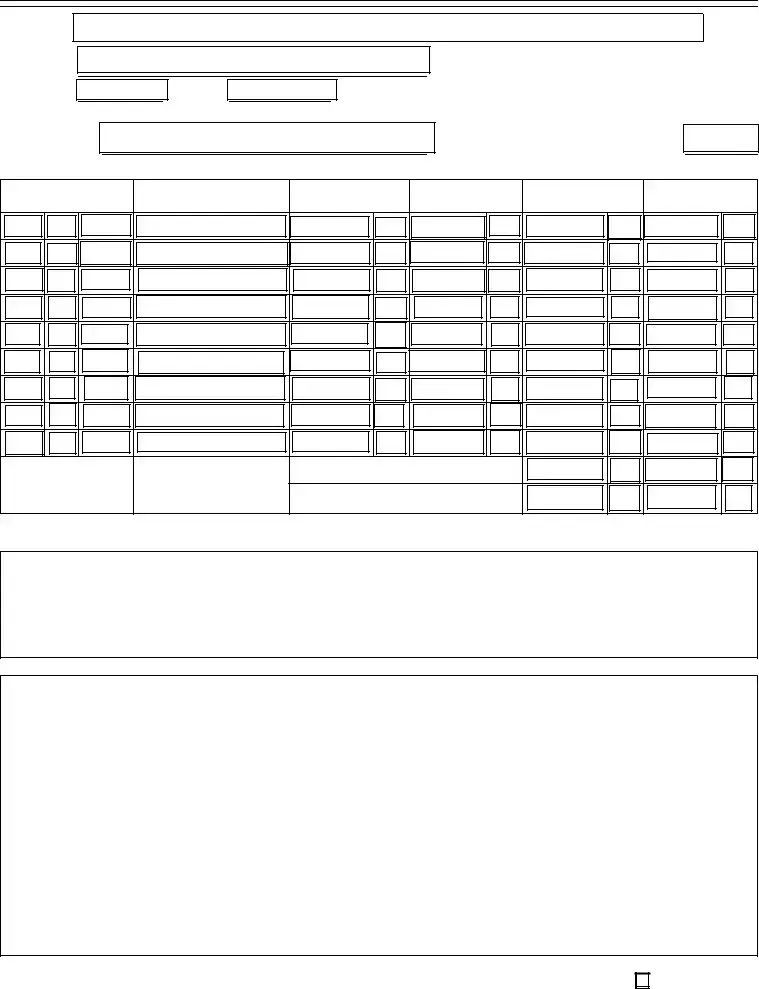

FORM CONN.

CORRECTION OF

EMPLOYER CONTRIBUTION RETURN

PLEASE COMPLETE BOTH PAGES OF THIS RETURN

QUARTER |

|

|

|

YEAR |

|

|

|

|

|

CONN. REG. NO.:

CORPORATE NAME OR

TRADE NAME

CONNECTICUT DEPARTMENT OF LABOR EMPLOYER TAX ACCOUNTING UNIT 200 FOLLY BROOK BOULEVARD WETHERSFIELD, CT

Pay Online at: www.ct.gov/doltax

ADDRESS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

COLUMN A |

|

COLUMN B |

COLUMN C |

|

COLUMN D |

|||||

|

|

|

|

|

ORIGINAL |

|

CORRECTED |

INCREASE |

|

DECREASE |

|||||

1 |

CONTRIBUTION RATE |

% |

|

RETURN |

|

RETURN |

(Difference between Column |

|

(Difference between Column |

||||||

|

|

|

|

|

|

|

|||||||||

|

See original return filed for contribution rate. |

|

(Enter below amounts |

|

|

|

A and Column B when |

|

A and Column B, when |

||||||

|

|

reported on original return for |

|

|

|

Column B is larger) |

|

Column B is smaller) |

|||||||

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

corresponding items) |

|

|

|

|

|

|

|

|

|

|

2 |

TOTAL GROSS WAGES PAID TO ALL EMPLOYEES FOR WORK |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

||||

PERFORMED IN CONNECTICUT THIS QTR |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

TOTAL GROSS WAGES PAID DURING THIS QUARTER TO EACH |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

||||

EMPLOYEE IN EXCESS OF THE LIMITATION FOR THE |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

CALENDAR YEAR |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

4 |

TOTAL TAXABLE |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

||||

DIFFERENCE BETWEEN COL. A AND B IN COL. C OR D. |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

CONTRIBUTION OR CREDIT DUE: SEE INSTRUCTIONS BELOW. |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

INTEREST DUE. IF CORRECTION RESULTED IN AN INCREASE IN CONTRIBUTION (LINE 5, COLUMN C), ENTER INTEREST |

|

|

|

********** |

|

|||||||||

|

|

|

|

||||||||||||

DUE IN COLUMN C. SEE INSTRUCTIONS BELOW. |

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

IF INCREASE IN CONTRIBUTIONS DUE (ITEM 5C), ENTER PENALTY DUE, IF ANY, IN COLUMN C. SEE INSTRUCTIONS |

|

|

|

********** |

|

|||||||||

|

|

|

|

||||||||||||

BELOW. |

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

TOTAL ADDITIONAL AMOUNT DUE – SUM OF ITEMS 5C, 6C AND 7C. PAY ONLINE AT: WWW.CT.GOV/DOLTAX |

|

|

|

********** |

|

|||||||||

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9EXPLAIN REASON FOR CORRECTION

PHONE NUMBER (

)

TITLE

DATE

HOW TO PREPARE FORM CONN.

HEADING: Enter QUARTER/YEAR, Connecticut Registration Number, Employer Trade Name, Name of Owners, Partners, or Corporate name (if other than trade name) and your Mailing address

Item 1: Contribution Rate – enter Contribution Rate for this quarter. If Rate has been corrected, use Corrected Rate.

Item 2: Enter Column “A” the Gross Wages Listed on the Original Return. Enter in Column “B” the correct amount of Gross Wages. If

Column “B” is larger than Column “A”, enter the difference in Column “C”. If Column “B” is smaller than Column “A”, enter the difference in Column “D”.

Item 3: Excess Wages – Wages paid during quarter in excess of the limitation for the calendar year. Enter the Column “A” excess wages as listed on original Return. Enter in Column “B” the correct amount of Excess Wages. Enter the Difference between Columns “A” and “B” in appropriate Column “C” or “D”.

Item 4:

Item 5:

Item 6:

Item 7:

Item 8: Item 9:

Item 10:

Item 2 minus Item 3

Enter in Column “A” the taxable Wages subject to contributions as listed on the Original Return.

Enter in Column “B” the correct amount of Taxable Wages subject to contributions. Enter difference between Columns “A” and “B” in the appropriate Column “C” and “D”.

Enter in Column “A” the Contributions listed on the Original Return. Enter in Column “B” the amount of Contributions due on corrected wages by multiplying Item 4B by the Contribution rate in Item 1. If Column “B” is larger than Column “A”, it represents Additional Contributions Due, and the difference should be entered in Column “C” (INCREASE). IF Column “B” is less than Column “A”, it represents an Overstatement of Contributions and the difference should be entered in Column “D”

(DECREASE). If a DECREASE, a refund may be issued, if applicable.

Enter in Column “C” the interest due on the additional contributions due. Multiply item 5C by the appropriate interest rate. One percent interest is charged for each month, or part thereof, that this return is filed late. Example: If the quarter being filed is the first quarter, the due date is April 30. Beginning May 1st , calculate 1% interest due. On June 1, 2% interest; on July 1, 3% interest; etc. If it is a second quarter return, interest begins to accrue August 1st; for a 3rd quarter return, November 1st; and for a 4th quarter return, February 1st .

Enter in Column “C” any penalty on the additional contributions due. A penalty of ten percent (10%) or fifty dollars ($50), whichever is greater, is assessed if the balance of contributions due is not paid within thirty days of the due date. Penalty dates: 1st quarter

Enter the total Amount due (the Sum of Items “5C”, “6C” and “7C”). Pay online at: www.ct.gov/doltax

Explain the reason for Correction fully. If additional space is required, attach a letter furnishing all facts and refer to the letter in this space.

This correction return must be signed by a responsible and duly authorized person and mailed to the address listed above. Any payment due, however, must be made online at www.ct.gov/doltax.

Filling out the UC-2 Connecticut form can be a straightforward process, but many individuals make common mistakes that can lead to delays or complications. One frequent error occurs in the heading section. People often forget to include all necessary information, such as the Connecticut Registration Number or the Employer Trade Name. Omitting any of these details can cause the form to be rejected, requiring resubmission and potentially delaying corrections.

Another mistake involves the employee information. Some individuals mistakenly list employees who are not part of the correction. The instructions clearly state to list only those employees whose wages are being corrected. Including additional names can complicate the processing of the form and may lead to confusion during audits.

Accuracy is crucial when entering wages. A common oversight is entering incorrect figures for the original wages or the correct wages. This can occur due to simple typos or miscalculations. If the numbers do not match the original Employee Quarterly Earnings Report, the corrections will not be processed correctly, leading to further discrepancies.

Additionally, many people neglect to provide a detailed explanation for the correction in Item 9. This section is vital for clarifying why the correction is necessary. A vague or incomplete explanation can result in additional questions from the Department of Labor, prolonging the resolution process.

Another common error is failing to sign the form. The instructions specify that the correction return must be signed by a responsible and duly authorized person. Without a signature, the form is incomplete and cannot be processed, which may lead to penalties or further complications.

Lastly, individuals often overlook the importance of keeping copies of submitted forms. While the instructions suggest retaining a copy for your files, many people skip this step. Having a copy is essential for reference in case any issues arise later, ensuring that you have documentation of what was submitted.

Filling out the UC-2 Connecticut form can seem daunting, but understanding the key aspects can simplify the process. Here are some essential takeaways to keep in mind:

By following these guidelines, you can navigate the correction process with confidence. If you have questions or need further assistance, don't hesitate to reach out to the Employer Tax Accounting Unit for clarification.

The UC-2 Connecticut form is similar to the IRS Form 941, which is used by employers to report income taxes, Social Security tax, and Medicare tax withheld from employee paychecks. Like the UC-2, Form 941 requires employers to provide detailed wage information and tax calculations for each quarter. Both forms serve to correct previously submitted information, ensuring that any discrepancies are addressed promptly. Employers must file Form 941 quarterly, much like the UC-2, reinforcing the importance of accurate reporting for tax compliance.

Another document akin to the UC-2 is the IRS Form 940, which is the Employer's Annual Federal Unemployment (FUTA) Tax Return. This form is used to report and pay unemployment taxes to the federal government. Similar to the UC-2, it requires employers to calculate their tax liability based on employee wages. Both forms emphasize the need for accurate reporting of wages to ensure compliance with unemployment tax obligations, highlighting the interconnectedness of state and federal tax systems.

The UC-2 is also comparable to the Connecticut Form CT-941, which is the state equivalent of the federal Form 941. This form is used to report Connecticut income tax withheld from employees’ wages. Like the UC-2, the CT-941 must be filed quarterly and requires detailed information about wages and taxes withheld. Both forms play a crucial role in ensuring that employers meet their state tax obligations, reinforcing the importance of accurate wage reporting.

For employers requiring verification of their hires, the essential employment verification document is crucial to confirm employment eligibility and legal compliance.

Another similar document is the IRS Form W-2, which reports an employee's annual wages and the taxes withheld from their pay. While the UC-2 focuses on quarterly contributions and corrections, both forms aim to provide accurate financial information to tax authorities. The W-2 is essential for employees to file their personal income tax returns, just as the UC-2 is vital for employers to maintain compliance with state unemployment insurance requirements.

The UC-2 form shares similarities with the IRS Form 1099-MISC, which is used to report payments made to independent contractors. Both forms require accurate reporting of payments and taxes, ensuring compliance with tax regulations. While the UC-2 is specific to employer contributions for unemployment insurance, the 1099-MISC addresses different types of income, highlighting the diverse landscape of tax reporting requirements for businesses.

Lastly, the UC-2 is akin to the Connecticut Form CT-1040, which is the state income tax return for individuals. While the UC-2 focuses on employer contributions, both forms require detailed financial information and are essential for tax compliance. The CT-1040 ensures that individuals report their income accurately, similar to how the UC-2 ensures that employers report their contributions correctly, emphasizing the importance of accountability in the tax system.